Pricing the

Keynesian Beauty Contest.

Leveraging institutional-grade quantitative models and the St. Gallen "Auction Price Mechanism" to extract alpha from the $65B art market.

Subjectivity is an Asset Class

We operationalize the St. Gallen "Auction Price Mechanism." We don't rely on taste; we model determinants like canonization, freshness, and momentum.

Correcting Expert Bias

Our models identified a 15-20% conservative bias in expert estimates. By neutralizing this anchor, we reduce valuation error by 36%.

Quantifying Upside Risk

We replace single-point estimates with Bayesian Confidence Intervals, isolating "Safe Value" assets from "High Variance" opportunities.

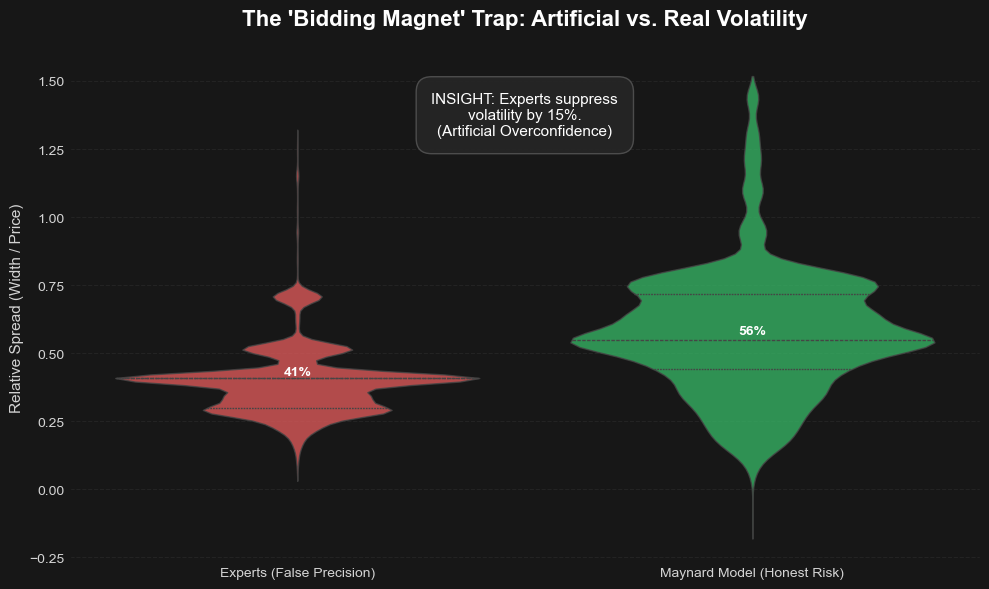

The "Bidding Magnet"

Trap.

Experts intentionally suppress estimates to induce bidding wars. This "sales tactic" creates artificially tight spreads that fail to account for real financial risk.

Artificial Tightness

By anchoring estimates low (median spread $2,000), experts signal false safety. This works for marketing, but fails for valuation—missing the true price 60% of the time.

Honest Volatility

Our model refuses to lie about risk. We widen the bracket (median spread $4,000) to honestly capture the "Breakout Potential" of the asset, achieving 79.9% reliability.

Sales Tactics vs. Financial Reality

The Team

Tier-1 financial experience meets deep technical expertise.